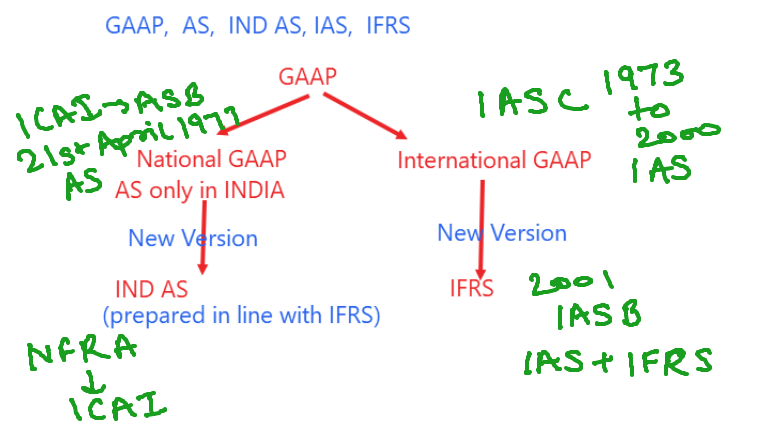

GAAP (generally accepted accounting principles) is a collection of commonly-followed accounting rules and standards for financial reporting. The acronym is pronounced "gap." GAAP specifications include definitions of concepts and principles, as well as industry-specific rules.

Best Coaching for CBSE UGC NET 8 July 2018 https://goo.gl/i34Npu Complete Course for CBSE UGC NET Paper 1

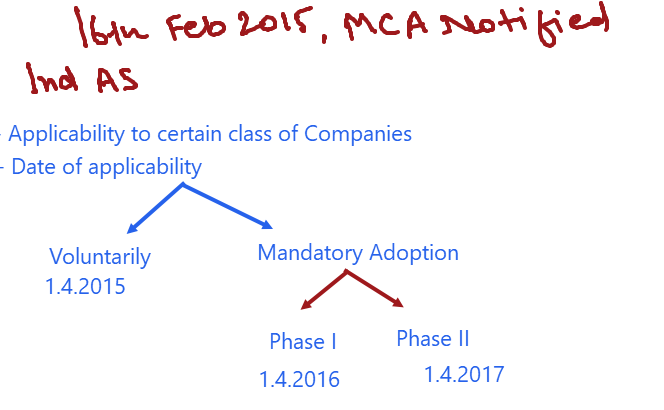

Section 2(2): “Accounting Standards” means the standards of accounting or any addendum thereto for companies or class of companies referred to in section 133; (New Definition in the Companies Act, 2013)

Section No.

|

Section Name

|

132

|

Constitution of National Financial Reporting Authority

|

133

|

Central Government to prescribe accounting standards

|

AS TRICKS: After Completing Studies, A wants to start a New Business....

So he makes various

Plans and POLICIES

regarding the new

Business.

AS-2 Valuation of INVENTORIES (IndAS 2)

He decides to acquire

various INVENTORIES

for his new business.

AS-3 CASH FLOW Statements (IndAS 7)

Because he knows that

by selling inventories he will get CASH FLOWS

AS-4 CONTINGENCIES and Events occurring after Balance Sheet Date (IndAS 10)

But he is not aware of various

CONTINGENCIES and his

stocks were destroyed.

AS-5 Net Profit or Loss for the Period, PRIOR PERIOD items and Changes in Accounting Policies (IndAS 8)

The Fire took place because of

wrong electrical wiring done in

the PRIOR PERIOD

AS-6 DEPRECIATION Accounting (IndAS 16)

Due to Fire, all his Assets

get DEPRECIATED

AS-7 CONSTRUCTION Contracts (Revised 2002) (IndAS 11)

After the Business Loss, he is

now going to CONSTRUCT a

new Business.

AS-9 REVENUE Recognition (IndAS 18)

And it is clear that

only after Constructing

a new business, he will generate REVENUE

AS-10 Accounting for FIXED ASSETS (IndAS 16)

So he starts acquiring

FIXED ASSETS for

his new business.

AS-11 The Effects of Changes in FOREIGN EXCHANGES Rates (Revised 2003) (IndAS 21)

As he lost everything in

that Fire Accident. So he

is now taking a Loan from

FOREIGN EXCHANGE

AS-12 Accounting for Government GRANTS (IndAS 20)

He is very closed to MODI,

hence Govt. gives him

GRANT too, to re-start his

business

AS-13 Accounting for INVESTMENTS (IndAS 40)

Now he has Money

received from Foreign

Loan and Grant, so this

time, he decided to make

INVESTMENT wisely.

AS-14 Accounting for AMALGAMATIONS (IndAS 103)

As he made good

Investments, his business

is now making Profits and

therefore receives an offer

of AMALGAMATION

from Mukesh Ambani.

AS-15 EMPLOYEE BENEFITS (IndAS 19)

When the EMPLOYEES

informed about the

Amalgamation, they

shouted for the settlement

of their outstanding

BENEFITS.

AS-16 BORROWING Costs (IndAS 23)

To settle the employee’s

benefits, he takes further BORROWING.

AS-17 SEGMENT Reporting (IndAS 108)

Before Amalgamation, it

was observed that one of

the SEGMENT is

performing negatively.

AS-18 RELATED PARTY Disclosure (IndAS 24)

The Segment Report reveals that

abnormal payments were made

to the RELATED PARTY.

AS-19 LEASES (IndAS 17)

The abnormal payments

made to the Related

Parties was for high

LEASE rentals.

Hence decided to close it

down.

AS-20 EARNINGS PER SHARE (IndAS 33)

After closing the Lease

Segment, the EPS is

increased and all the

ShareHolders are

Happy.

AS-21 CONSOLIDATED Financial Statements (IndAS 27)

Now at the year end,

he prepares his

CONSOLIDATED

Financial Statements.

AS-22 Accounting for TAXES on Income (IndAS 12)

After closing the accounts,

proper TAX has been paid

to the Govt.

AS-23 Accounting for Investment in ASSOCIATES in Consolidated Financial Statements (IndAS 28)

The company has not

paid any tax for his ASSOCIATES businesses.

AS-24 DISCONTINUING Operations (IndAS 105)

Because the Associate

business is now DISCONTINUED.

AS-25 INTERIM Financial Reporting (IndAS 34)

To Cross Check the

authenticity of that

discontinued Business,

INTERIM reports are

reviewed.

AS-26 INTANGIBLE Assets (IndAS 38)

After all the efforts,

the business has made

its own Goodwill

(INTANGIBLE)

AS-27 Financial Reporting of Interests in JOINT VENTURE (IndAS 31)

Due to his Goodwill, he is

now going to enter into a

very Big Project through

JOINT VENTURE.

AS-28 IMPAIRMENT of Assets (IndAS 36)

After completing the Joint

Venture, the assets are not

justifies the Book Value of

few of the Assets hence

results IMPAIRMENT of

Assets.

AS-29 Provisions, CONTINGENT Liabilities and CONTINGENT Assets (IndAS 37)

During the Joint Venture a

Labour got injured and filed a

case against the company, which

is creating a CONTINGENT

Liability for the business.

AS-30 Financial Instruments : Recognition and MEASUREment (IndAS 39)

The amount of money payable to the labour is

MEASURE by the Court

AS-31 Financial Instruments : PRESENTation (IndAS 32)

And an order has been passed to PRESENT the

required money to the Labour

AS-32 Financial Instruments : DisCLOSURE (IndAS 107)

For the CLOSURE of the case.

AS 1 Disclosure of Accounting Principles

AS 2 Valuation of Inventories Limited Revision

AS 3 Cash Flow Statements

AS 4 Contingencies and Events Occurring After the Balance Sheet Date

AS 5 Net Profit or Loss for the Period, Prior Period Items and Changes in Accounting Policies

AS 6 Depreciation Accounting

AS 7 Construction Contracts (Revised 2002)

AS 9 Revenue Recognition

AS 10 Accounting for Fixed Assets

AS 11 The Effects Of Changes In Foreign Exchange Rates (Revised 2003) Limited Revision

AS 12 Accounting for Government Grants

AS 13 Accounting for Investments

AS 14 Accounting for Amalgamations

AS 15 Employee Benefits (Revised 2005)

AS 16 Borrowing Costs

AS 17 Segment Reporting

AS 18 Related Party Disclosures

AS 19 Leases Limited Revision

AS 20 Earnings Per Share

AS 21 Consolidated Financial Statements Limited Revision

AS 22 Accounting for taxes on income

AS 23 Accounting for Investments in Associates in Consolidated Financial Statements Limited Revision

AS 24 Discontinuing Operations

AS 26 Intangible Assets Limited Revision

AS 27 Financial Reporting of Interests in Joint Ventures Limited Revision

AS 28 Impairment of Assets Limited Revision

AS 29 Provisions, Contingent Liabilities and Contingent Assets Limited Revision

AS 30 Financial Instruments: Recognition and Measurement Withdrawn in November 2016

AS 31 Financial Instruments: Presentation Withdrawn in November 2016

Indian Accounting Standards Tricks

Ind As No. Name of Indian Accounting Standard

Ind AS 103 Business Combination

Ind AS 105 Non-Current Assets Held for Sale and Discontinued Operations

Ind AS 106 Exploration for and Evaluation of Mineral Resources

Ind AS 107 Financial Instruments: Disclosures

Ind AS 108 Operating Segments

Ind AS 109 Financial Instruments

Ind AS 110 Consolidated Financial Statements

Ind AS 111 Joint Arrangements

Ind AS 113 Fair Value Measurement

Ind AS 1 Presentation of Financial Statements

Ind AS 2 Inventories

Ind AS 7 Statement of Cash Flows

Ind AS 8 Accounting Policies, Changes in Accounting Estimates and Errors

Ind AS 10 Events after Reporting Period

Ind AS 11 Construction Contracts

Ind AS 12 Income Taxes

Ind AS 16 Property, Plant and Equipment

Ind AS 17 Leases

Ind AS 19 Employee Benefits

Ind AS 20 Accounting for Government Grants and Disclosure of Government Assistance

Ind AS 21 The Effects of Changes in Foreign Exchange Rates

Ind AS 23 Borrowing Costs

Ind AS 24 Related Party Disclosures

Ind AS 27 Separate Financial Statements

Ind AS 28 Investments in Associates and Joint Ventures

Ind AS 29 Financial Reporting in Hyperinflationary Economies

Ind AS 32 Financial Instruments: Presentation

Ind AS 33 Earnings per Share

Ind AS 34 Interim Financial Reporting

Ind AS 36 Impairment of Assets

Ind AS 37 Provisions, Contingent Liabilities and Contingent Assets

Ind AS 41 Agriculture

Teaching Aptitude: https://goo.gl/UF2ojY

Research Aptitude: https://goo.gl/TgyqyK

ICT- Computer Aptitude :https://goo.gl/7smZNu

Higher Education: https://goo.gl/3dSkPn

If any one wants to get PDFs by Navclasses then click here: https://www.facebook.com/groups/navclasses/files/

Join on FB Group: https://www.facebook.com/groups/navclasses/

Like Fb Page: https://www.facebook.com/navclassesonline

Teaching Aptitude: https://goo.gl/UF2ojY

Research Aptitude: https://goo.gl/TgyqyK

ICT- Computer Aptitude :https://goo.gl/7smZNu

Higher Education: https://goo.gl/3dSkPn

If any one wants to get PDFs by Navclasses then click here: https://www.facebook.com/groups/navclasses/files/

Join on FB Group: https://www.facebook.com/groups/navclasses/

Like Fb Page: https://www.facebook.com/navclassesonline

Comments

Post a Comment